Consumers are reducing the demand for credit cards, and the Fed is not amused.

By Wolf Richter for WOLF STREET.

Consumers as a whole have declined massively on Pandemic credit card applications; and also withdrew when they applied for a higher credit limit for the credit cards they already had. And a higher percentage of those who applied for a credit card or a higher credit limit were turned down. These are some of the findings of the New York Fed’s access to credit survey conducted today. The survey on access to credit is conducted three times a year (also in February and June).

The notion that consumers reduce the reduction in credit card loans causes Fed consumption; high interest rates, in many cases over 20%, in an average interest rate close to zero, is where banks make extraordinary profits. And consumers, those who can afford the least, pay by the nose for these bank profits.

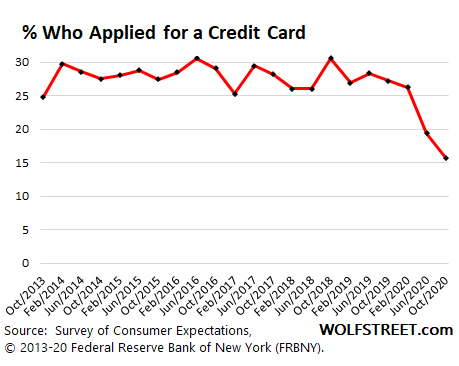

Only 15.7% of consumers said they had applied for a credit card in the last 12 months, down from 25% to 31% before the Pandemic and down from 26.3% in February and by far the most decreased from the survey data back to 2013:

The Fed in New York, which, like all 12 Federal Reserve banks, is owned by the largest financial institutions in its district, laments: “The latest credit access survey reveals the strong pandemic on credit markets. For consumption”.

Consumers have also reduced their demand for car loans, but only slightly compared to the steep cuts in credit card applications, the survey found.

And only 7.1% of consumers requested a higher credit limit for the credit cards they already held, the lowest of the survey data and down from 8% to 15% in previous years.

So there is clearly a problem with consumers not falling under the Fed. One reason could be that credit card interest rates typically remain high, even though the Fed is committed to historically lowering the interest rate, which eliminates depositors and holders of treasury securities who earn the tiny interest-free on their funds.

To borrow 10%, 20%, 25% or God forbid 30% – credit card issuers have no obligation to go there – in this low-interest environment, people should be ultra-desperate consumers or, well , only good consumers in the eyes of the Fed, handing over hard-earned money to banks in the form of usurious interest.

But of those people who applied for a credit card, probably to make the Fed happy, 21.3% were rejected, the third highest rejection rate in the data series:

And 37.1% of those who applied for a higher credit limit were rejected:

These higher rejection rates could indicate a combination of two things: one, a shift in the mix of applications to consumers with higher debt burdens and more insecure credit histories, while other consumers do not apply, thus increasing rates. global rejection; and tighter subscription from banks.

These credit card consumer findings add another piece to the puzzle of why credit card balances have generally fallen in a historic way and for the Fed in an annoying way.

Credit card balances and other revolving credit balances in October decreased by 10.3% compared to a year earlier, the largest year-on-year decline in credit card data from the first days to $ 943 billion (seasonally adjusted, red line), a balance sheet first seen in August 2007, despite 13 years of inflation and population growth:

During the financial crisis, when credit card balances fell from June 2008 to May 2011 on a seasonally adjusted basis (the green line above), there was another huge factor that plays a role: deaths and subsequent amortization of creditors. Consumers have massively paid off their credit cards – in 2009, almost 14% of all credit card balances were delinquent – and many depreciated, moving away from their debts and addressing the consequences.

But this is not happening now. New delinquent credit card balances declined in the second and third quarters, fueled by a combination of extensive and alleged deferral programs and incentive money:

What we are witnessing are the bizarre effects of the Pandemic stimulus expand-and-claim economy. And there may be a flicker in the minds of consumers – yet I doubt it – that loans at 10% or 20% in a near-zero interest rate environment are only good for the bank’s shareholders, and otherwise it’s a stupid deal. and that it is time to starve to that great source of income, paying that debt with high interest.

Stimulus Fatigue is installed. The second month of declining retail sales in a row. But online sales have set a new record, if at all. Read... Where the Americans shattered and where they retreated into 13 whiplash charts

Do you enjoy reading WOLF STREET and would like to support it? Using ad blockers – I understand why – but I want to support the site? You can donate. I really appreciate it. Click on the beer mug and iced tea to learn how:

Would you like to be notified by email when WOLF STREET publishes a new article? Sign up here.

![]()